us japan tax treaty technical explanation

Japan Tax Treaty. ON NOVEMBER 6 2003.

Tax Treaty Limitation On Benefits Lob Form W8 Ben E International Tax Blog

Department of the Treasury Technical Explanation of the most recent 2007 protocol amendments to the USCanada tax treaty.

. Here is the wording from the US Treasury Technical Explanation of the treaty which I think supports this. The tax treaty with Brazil provides a 25 tax rate for certain royalties trademark. Real property interest also includes certain foreign corporations that have elected to be treated as US.

Some countries have estate tax treaties with the United States including Japan. The tax treaty was concluded mainly for the purpose of information exchange. Japan should consider my 401 k and my US private pension as retirement income for taxation purposes.

Estate tax treaty does change some of these rules so. This is a technical explanation of the Protocol signed at Washington on December 8 2004 the Protocol which amends the Convention Between the United States of America and the French Republic for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Estates Inheritances and Gifts signed at Washington. TAXES ON INCOME AND ON CAPITAL GAINS SIGNED AT WASHINGTON.

A protocol the Protocol to the US-Japan Tax Treaty the Treaty which implements various long- awaited changes entered into force on August 30 2019 upon the exchange of instruments of ratification between the Government of Japan and the Government of the United States of America. Technical Explanation PDF - 2003. Technically a tax treaty is referred to as a Bilateral Income Tax Treaty and millions of US.

Senate on july 16 and 17 approved resolutions of ratification of protocols signed during the administration of president obama that would amend the us. Under the Japan-US tax treaty if a resident of a Contracting State transfers any of the following assets the taxing rights on capital gains from such transfers are granted to the other Contracting State. 4 The term US.

However the WHT rate cannot exceed 2042 including the income surtax of 21 on any royalties to be received by a non-resident taxpayer of Japan under Japanese income tax law. TECHNICAL EXPLANATION OF THE UNITED STATES-JAPAN INCOME TAX CONVENTION GENERAL EFFECTIVE DATE UNDER ARTICLE 28. Film royalties are taxed at.

Ary 24 2004 Technical Explanation the Technical Explanation is the official guide to the new Treaty. On July 17 2019 the US. The Technical Explanation is viewed by officials practitioners and scholars as an official guide to that particular convention.

Taxpayers are impacted by the language found within International Tax Treaties. Treasury Department issues a different Technical Explanation for each tax treaty that the United States enters into. In the table below you can access the text of many US income tax treaties protocols notes and the accompanying Treasury Department tax treaty technical explanations as they become publicly available.

How to Read and Analyze a Tax Treaty. Protocol PDF - 2003. These treaties may change the default taxation rules that the United States or another country would apply to people who file tax returns in that country.

My US taxes should be the same whether I retire in the US or Japan. Article 11 provides that in cases involving a special relationship between the payor and the beneficial owner where the amount of interest paid exceeds the amount that would otherwise have been agreed upon in the absence of the special relationship then the treaty rate applies only to the last-mentioned amount that is the arms length interest payment as it is referred to. This technical explanation is an official guide to the protocol memorandum of understanding and exchange of notes.

Us japan tax treaty technical explanation. Is or was on good terms at the time the treaty was entered into. This is based on the treatys statement that US reserves right to tax citizens regardless of treaty provisions.

And a foreign country in which the US. Country under the provisions of a tax treaty between the United States and the foreign country and the individual does not waive the benefits of such treaty applicable to residents of the foreign. 1 january 1973 CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF JAPAN FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES.

Department of the treasury technical explanation of the protocol signed at washington on january 14 2013 amending the convention between the government of the united states of america and the government of japan for the avoidance of double taxation and the prevention of fiscal evasion with. It reflects the policies. Tax Treaty is signed between the US.

Us germany tax treaty technical explanation. Technical Explanation PDF - 1971. The Technical Explanation is an official guide to the Convention.

Corporations for this purpose. Real property situated in the other Contracting State. Protocol Amending the Convention between the Government of the United States of America and the Government of Japan for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Income PDF.

This article uses the current United StatesCanada income tax treaty text posted by Canadas Department of Finance. 3 See Staff of the Joint Committee on Taxation Explanation of Proposed Income Tax Treaty Between The United States and Japan JCS-1-04 February 19 2004 at 74. B in the case of the united states.

Key provisions include 1 zero rate with-holding on certain inter-corporate dividends on all royalties and on cer-tain interest including interest derived by banks insurance companies and other financial institutions. Parent entity hereinafter Technical Explanation of Japan-US. Technical explanation of the united states-japan income tax convention general effective date under article 28.

Im reading Article 17 of the US-Japan Tax Treaty about private pensions and it appears to be saying that income from US company-sponsored pensions and 401kIRA accounts funded by non-government employment are only taxable in the US. This is a technical explanation of the Convention between the Government of the United States of America and the Government of Japan for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income signed at Washington on. This article also refers to the authoritative US.

1 The Protocol which was approved by the United States Senate Foreign Relations Committee on June 25 2019 contains amendments to the existing income tax treaty between the. Please note that treaty documents are posted on this site upon signature and prior to ratification and entry into force. Convention Between the United States of America and Japan for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income signed at Tokyo on March 81971.

Technical explanation of the protocol between the united states of america and the federal republic of germany signed at washington on december 14 1998 amending the convention between the united states of america and the federal republic of germany for the avoidance of double taxation with respect. Senate voted in favor of ratifying the Protocol between the United States and Japan that was signed by both countries on January 24 2013. Income Tax Treaty PDF- 2003.

2

2

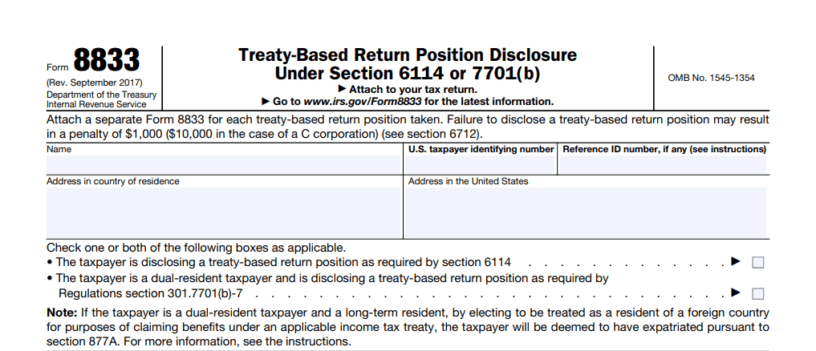

Form 8833 Tax Treaties Understanding Your Us Tax Return

2

2

2

Deloitte Tax Hand

How To Design A Regional Tax Treaty And Tax Treaty Policy Framework In A Developing Country In Imf How To Notes Volume 2021 Issue 003 2021

Unraveling The United States Japan Income Tax Treaty And A Closer Look At Article 4 6 Of The Treaty Which Limits The Use Of Arbitrage Structures Sf Tax Counsel

2

International Taxation

Japan United States International Income Tax Treaty Explained

Tax Treaty Limitation On Benefits Lob Form W8 Ben E International Tax Blog

International Taxation

2

2

Ecm Day Is Here Armstrong Economics Economic Events Economics Us Stock Market

Tax Treaty Limitation On Benefits Lob Form W8 Ben E International Tax Blog

International Taxation